Otso Monthly - June 2026

How did we perform?

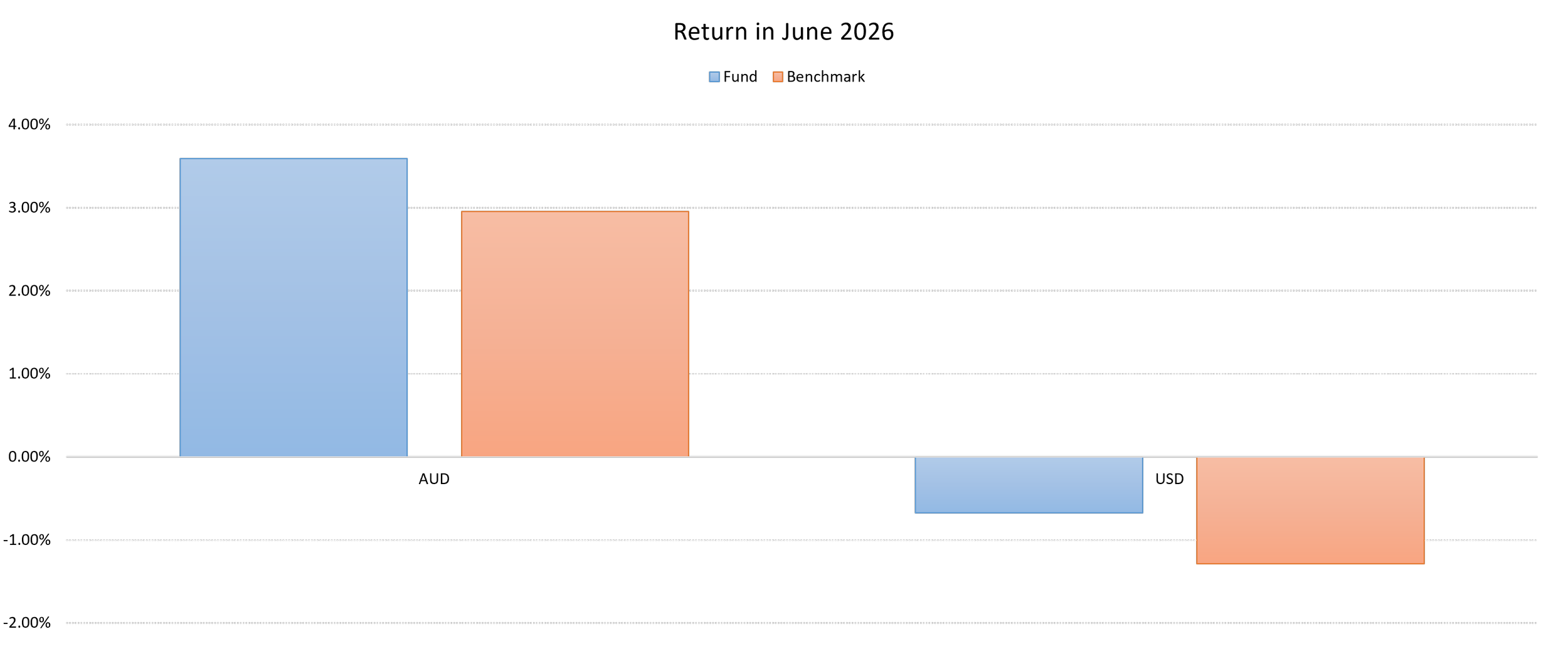

We outperformed the benchmark (S&P500, as proxied by the SPY). We delivered 3.59% in AUD terms (vs benchmark of 2.96%), and -0.67% in USD terms (vs benchmark of -1.28%). The solid performance was encouraging, and suggests that we may be right-sized for the current market risk appetite. We are also particularly interested in the opportunities that companies such as SpaceX offer for overlay-related strategies. However, as always, it would form only one part of a broader portfolio.

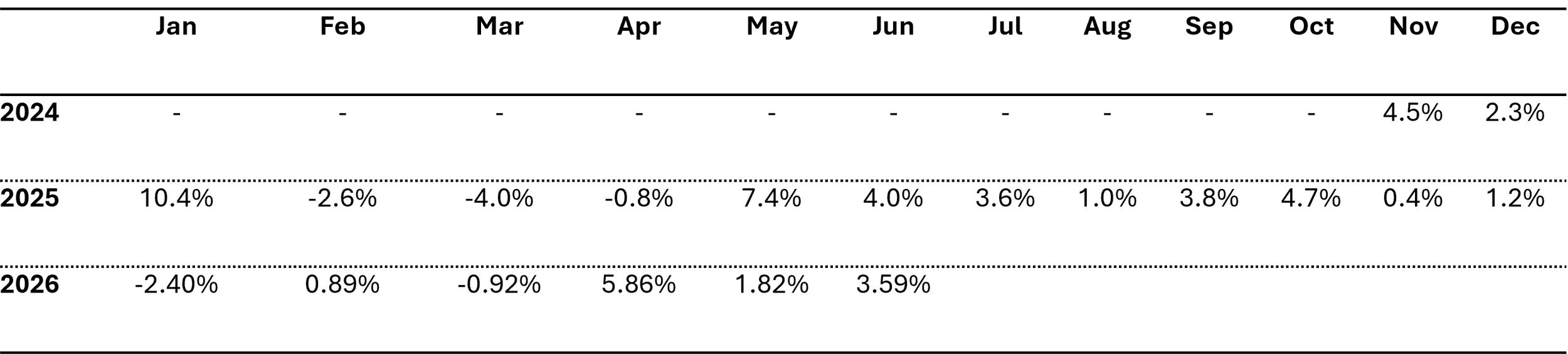

Our performance over time has also been strong, delivering consistently solid returns since inception. However, past performance need not imply future performance.

What happened in June?

June closed the book on a remarkable first half, though the month itself marked a subtle turning point. After two months of near vertical gains, US equities took a breather and, more importantly, began to change character. The S&P 500 fell 0.7% in June but still delivered a 15.3% gain for the second quarter, its largest quarterly gain in six years.

Beneath that modest headline decline, something healthier was happening. Leadership broadened. The S&P 500 Equal Weight Index advanced 2.4%, and the small-cap Russell 2000 rose 3.7%, ending the month up nearly 23% on the year and capping its best first-half performance since 1991.

The AI trade splits in two

The dominant story of the year finally showed some internal tension. June saw a divergence within the AI trade, with semiconductor stocks continuing to benefit from robust demand while the hyperscalers funding much of the AI buildout came under pressure.

The numbers were striking. The PHLX Semiconductor Index rose 11%, capping a record 88% quarterly gain, while the Magnificent 7 cohort experienced its largest monthly decline in more than a year.

Investors did not flee so much as rotate. Throughout June, investors chose to shift to other market sectors rather than outright sell, a sign that confidence remained despite uncertainty. Industrials, healthcare, and financials outperformed as technology cooled.

The capital spending behind all this remains staggering. Consensus now points to the largest cloud providers committing well over $700 billion this year, a figure that has crept steadily higher throughout 2026 and is starting to spill into industrial and energy suppliers.

A new Fed, a new tone

June brought the first meeting under new Federal Reserve Chair Kevin Warsh, and it set a distinctly hawkish tone. The Fed held its benchmark rate steady in the 3.5% to 3.75% range, as expected.

The bigger news was the forward path. Updated projections showed a higher path for interest rates, prompting a hawkish shift in market expectations, with a 25 basis-point rate hike fully priced in by October.

This is a genuine regime change in sentiment. Earlier this year, markets expected cuts. Now they are debating hikes, driven by sticky inflation and the earlier commodity shock. Traders should note that the new Fed has also signaled leaner communications, giving the committee more room to move.

Oil eases as the Gulf calms

The geopolitical cloud that hung over spring began to lift. The month was marked by falling oil prices following the U.S.-Iran agreement.

That relief is real but fragile. Oil prices have fallen sharply, but further declines will likely hinge on a meaningful recovery in oil supply from the Persian Gulf. Restoring output from the region involves clearing the Strait of Hormuz, bringing crews back, and restarting production, all of which take time. Investors are pricing peace with caution, wary of periodic flare-ups.

A record for the IPO market

June delivered one of the largest capital-raising events in Wall Street history. SpaceX began trading at the Nasdaq on June 12, opening at $150 per share, roughly 11% above its $135 IPO price. The stock closed at $161, jumping 19% on its debut.

The scale was extraordinary. SpaceX sold 555.6 million shares for a $75 billion fundraise at a $1.77 trillion valuation, making it one of the largest US companies by market capitalization. One takeaway captured the moment well: AI is extraordinarily capital intensive, and capital formation is shifting toward equity. With Anthropic and OpenAI both moving toward the public market, the pipeline is far from empty.

The economy holds up

Underlying data stayed firm. Labor indicators were solid, with job openings expanding at their fastest pace in two years and payrolls beating expectations. Consumer sentiment improved as Middle East tensions eased. In short, the fundamentals gave investors room for optimism even against elevated oil and inflation.

The Australian context

Unfortunately, Australia’s economic competitiveness has nosedived. We are extremely constructive on the US relative to Australia and regard Australia as a moribund, parochial economy under the current leadership. Anthony Albanese and Jim Chalmers lied to Australians, especially investors. They specifically said they would not increase CGT. But, they have done so. These lies should be hung around their neck like a petard. The CGT hikes make Australia backward looking, rendering Australia’s tax rate the highest in the world absent appropriate planning and structuring, including through sub-investment-companies. This is why leading investors, such as Geoff Wilson, have flagged managed funds as an important avenue post-tax-hike.

Albanese and Chalmers lied, and not for a good reason. They claim that circumstances changed since they were elected. This is a lie. I know because I appeared at the Senate inquiry into CGT changes in early 2026. Excerpts from my testimony are here (https://youtu.be/T-AUJjYtFdQ?si=AyFGAkg4g_uIpY54). It is implausible that circumstances changed within six months of the election. To claim as such is to layer another lie on top of the existing lies.

Moreover, the increased CGT rates will take the CGT rate well over the Laffer peak, as I have modeled here (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6980978). Pointedly, the revenue-maximizing CGT rate when you ignore second order effects is 30-40% (https://www.aeaweb.org/articles?id=10.1257/aeri.20200535). But, if you add second order effects, the rate falls. Specifically, second order effects include fiscal spillovers from investing (stamp duty, payroll tax, corporate income tax) and growth due to investing. They also include the impact of higher CGT on lockin effects and capital flight (and deterring capital from arriving). In short, the revenue-maximizing CGT rate, when you incorporate these effects, is low. The welfare-maximizing rate is still lower, especially when we have regard to the profligacy with which the Australian government spends money.

We will continue to fight for investors in this context. We regard supporting the ALP, or the Teals (who also want higher CGT), as a breach of fiduciary duties to clients. Supporting either party would be to harm our clients.

Looking forward (another new fund?)

We will continue to address the Australian debacle and will keep our portfolio risk-exposure right-sized for the US situation. We are constructive on the US. We regard the US, which recently celebrated its 250th birthday, as the leading economy for investors.

We are also considering an alternative asset fund: specifically, we are considering an active timepiece fund. If you might be interested in such a fund, stay tuned for more information if/when it launches or reach out to us. It would be a pleasure to act for you in that asset class.