Otso Monthly - May 2026

How did we perform?

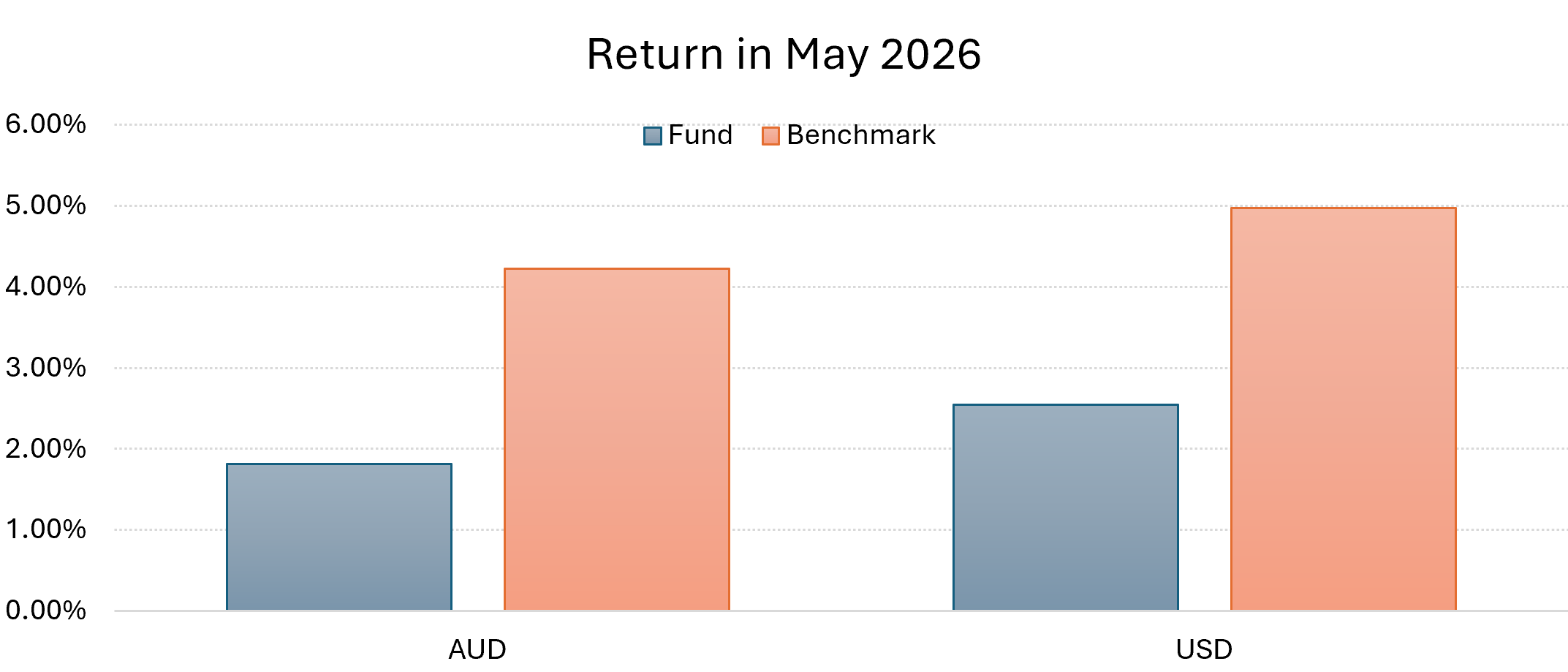

May was a solid, if underwhelming, month for Otso Capital. We delivered positive returns. However, our returns were ‘only’ 2.55% in USD terms, relative to a benchmark of ≈ 5% (S&P500 was 5.3%; SPY rose approximately 5%). In AUD terms, the story was similar. Owing to a non-trivial portion of the fund in AUD due to flows, we lost a little from currency fluctuations, delivering 1.82% return (vs benchmark of around 4.22%). This was not the outcome we had hoped for. While positive performance is better than negative performance, the underperformance is worth reflecting on.

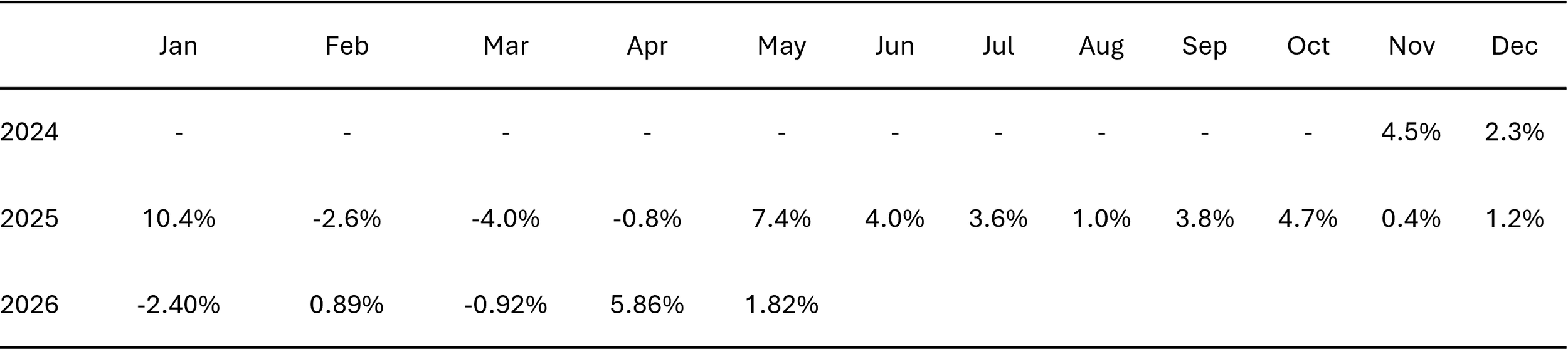

Performance over time in AUD

The question is then why is it that we underperformed the benchmark. This is only partly attributable to AUD holdings and currency fluctuations. It is largely attributable to the fund being “under-risked” at a time when the market increased significantly. We did not anticipate such significant gains given what we saw as an increasing likelihood of a Hawkish Fed (which turned out to be the case) and geopolitical tensions, which continue to manifest in curious market movements (viz., a positive reaction to talk of a US-Iran deal, but a seemingly muted reaction when the deal fails to eventuate). Nevertheless, it presents some learnings for positioning going forward.

What happened in May?

US equities staged a powerful, broad-based advance in May, with large-, mid-, and small-cap benchmarks all setting fresh all-time highs. The S&P 500 rose 5.3% and finished the month on a streak of nine consecutive weekly gains, an occurrence seen only four other times in the past 40 years. The index closed at a record 7,580.06 on May 29. Technology and growth names led decisively: the Nasdaq 100 (+10.6%) and Nasdaq Composite (+8.9%) outpaced the broader market for a second straight month, with the Composite ending near 26,973. The Dow crossed the 51,000 milestone for the first time, closing around 51,032, though its gain of roughly 2.8% trailed the others, reflecting its lighter weighting in the AI-driven leadership. Small caps participated as well, with the Russell 2000 up 4.4% (18.3% year-to-date) and the Russell Microcap Index up 6.6%, making it 2026's strongest performer at 22.1% year-to-date.

The rally was underpinned by an exceptional earnings season. First-quarter S&P 500 earnings growth tracked in the high-20% range year over year, more than double pre-season estimates, with revisions trending higher through the month. Sustained investment in artificial intelligence and digital infrastructure remained the dominant theme, with heavy capital spending on data centers, semiconductors, and cloud platforms supporting both revenue growth and margins.

Leadership was unusually narrow, however. Eight of the eleven S&P 500 sectors finished the month in negative territory, with Technology (+16.0%) the overwhelming leader. The semiconductor complex was the standout: the SOX index gained 22.1% in May on top of a 38.4% surge in April, a two-month return of 69.1% and its strongest such stretch since the index began in 1996. Outside tech, gains were modest, with Consumer Discretionary (+2.6%) and Health Care (+2.5%) the only other positive sectors. Energy (-5.6%) was the weakest as oil prices eased, followed by Utilities (-5.1%) and Consumer Staples (-3.2%); Financials fell 1.2%. This concentration is worth flagging as a risk, since headline index strength masked weak participation across much of the market.

The macro backdrop was mixed and is the main source of caution. Headline CPI rose to 3.8% year over year, the highest reading since May 2023, while core inflation ticked up to 2.8%. Producer prices climbed for a fourth straight month to 6.0% year over year, the highest since December 2022. The labor market stayed firm: the economy added 115,000 jobs, well above the 55,000 expected, and unemployment held at 4.3%. Leadership at the Fed changed hands during the month. Jerome Powell's eight-year tenure ended on May 15 and Kevin Warsh was sworn in as the 17th Fed Chair following Senate confirmation on May 14. Rates were left at 3.50 to 3.75%, and markets place better than a 99% probability on a hold at the June 17 meeting, while increasingly pricing the possibility of a hike later in 2026.

Bond markets reflected the sticky-inflation narrative. The 30-year Treasury yield made a marginal new cycle high near 5.2% before retracing to about 5%, a level that had acted as resistance through 2025 and into early 2026. The rise was most pronounced in the belly of the curve, flattening the 10s/2s spread. A resumption of that uptrend would be a key risk to watch, as it could pull the entire curve higher and pressure equity valuations.

Commodities and geopolitics were intertwined. Brent crude fell sharply, down 19.3%, on improving expectations for an Iran ceasefire and easing Middle East tensions, as traders unwound earlier supply-fear hedges. Gold slipped 1.7% while silver gained 2.1%, suggesting a possible bottoming after steep declines from February highs. Bitcoin fell 3.7% amid nine straight days of US spot-ETF outflows totaling roughly $2.8 billion, the longest withdrawal streak since the products launched in January 2024.

Single-stock highlights included Dell, which surged nearly 33%, its best day on record, after a top- and bottom-line beat and raised full-year guidance, and Apple, which advanced roughly 15% on the month and set repeated record highs. In primary-market news, SpaceX moved toward an IPO seeking a valuation of at least $1.8 trillion.

In short, May combined record-setting returns with genuine undercurrents of risk: stretched valuations, narrow breadth, sticky inflation, a rising long end, and a new Fed chair whose approach markets are still calibrating. Strong earnings and the AI capex cycle carried the month, but the gap between price action and the broader macro picture warrants attention heading into the second half.

Looking ahead

We are writing this in June. The concerns for our fund are largely closer-to-home. Labor’s appalling budget looks set to pass. This dramatically increases CGT for investments across most asset classes (except for your principal place of residence, and ESVCLPs). This is a significant concern. I appeared at the Wilson Asset Management (WAM) investor discussion forum in June to discuss this. You can see some of my remarks below.

My modeling also shows that the CGT rate hikes are a net negative for Australia. They will lower total revenue over the long term and reduce welfare. Labor’s rate maximizes revenue only if you ignore the elasticity of investment to the keep rate, fiscal spillovers from supporting business, growth effects driven by investment, the possibility that people will shift investments to lower taxed alternatives (i.e., principal place of residence) or offshore (i.e., move to New Zealand), and realized-gain lock-in issues. In short, if you ignore all ‘second order effects’ then maybe you can get a rate near Labor’s. But, once you consider these, the optimal rate is low, often near zero, and well below Labor’s proposed rate.

In terms of investing: the US-Iran conflict is steadily nearing a resolution. The Fed has been hawkish. However, the market appears to have adapted to this. We have anticipated this ‘risk on’ sentiment in our portfolio set up and are cautiously optimistic.