Otso Monthly - February 2026

How did we perform?

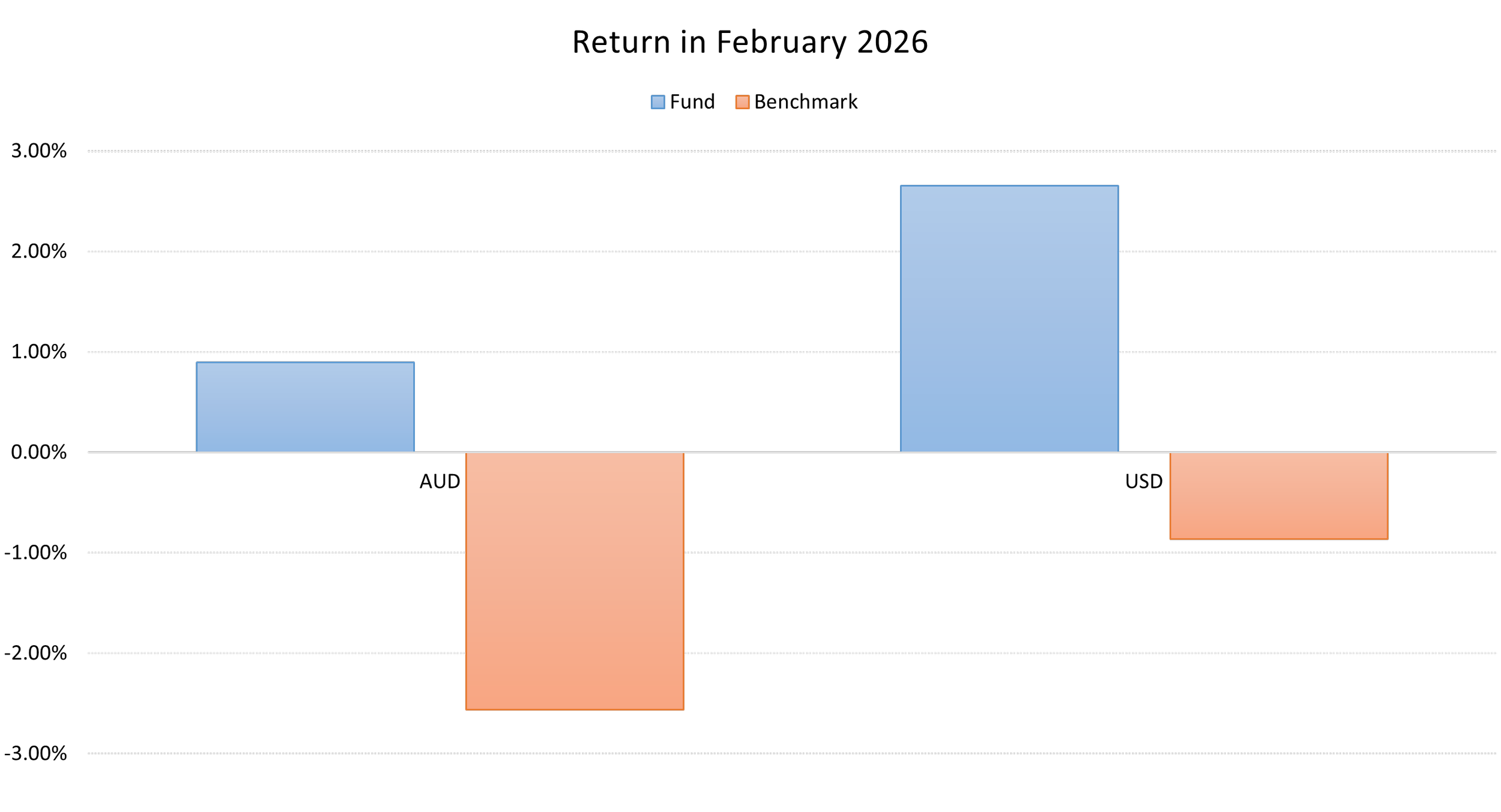

February was a solid month for the fund. After fees, we delivered 2.65% in USD terms (vs benchmark of -0.86%) and 0.89% in AUD terms (vs -2.56% benchmark). As this indicates, the AUD appreciated during February, weighing on AUD performance.

Performance has been strong since inception. However, past performance is not a guarantee of future performance.

What happened in February?

The market was somewhat unhappy in February: the S&P 500 fell around 0.8%. The Nasdaq fell around 2.3%. This was not a good outcome, being the worst return since March 2025. Interestingly, the equally weighted S&P 500 increased 3.5%. So, what explains these curious trends?

The SAASpocalypse! The anecdotal holy grail of revenue is recurring revenue. And what is more recurring than SAAS where customers are locked-in with painful switching costs? Well, it turns out that those lockins might be slightly less sticky than assumed. AI could enable customers to solve some of the use cases that had previously required expensive software subscriptions. This fear underscored some slippage in tech stocks.

The AI-focused stocks, however, did not gain significantly from the concerns that AI might replace jobs, however. Thus, while Block shed 4000 workers due to AI-related efficiencies, Nvidia also fell around 7.3%. This reflects growing concerns about hefty AI valuations and growth projections. It also reflects concerns about the viability of significant capital expenditures.

Meanwhile, energy, healthcare, and industrials all outpaced technology, confirming a broadening of market leadership. Small-cap stocks remained “attractive” at roughly 18 times earnings versus 28 times for large caps. Thus, the Russell 2000 performed better than the S&P500, ending up around 0.67%. However, within the Russell 2000, there is heterogeneity based n profitability.

Tariff chaos. Again. It was 12 months ago that President Trump started discussing tariffs in earnest, resulting in “Liberation Day” on 2 April 2025. However, one year on, and the US Supreme Court has struck down many of the tariffs.

The most consequential policy event of the month arrived on February 20, when the U.S. Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that the president lacked authority under the International Emergency Economic Powers Act to impose sweeping tariffs. The decision effectively dismantled the legal foundation for the reciprocal tariff regime that had imposed duties of up to 25–50% on goods from major trading partners including Canada, Mexico, and China.

Markets rallied on the news. The S&P 500 rose 0.69%, the Nasdaq gained 0.9%, and tariff-sensitive retailers surged—Etsy jumped 8%, Amazon and Wayfair each climbed 2%. However, the rally was tempered by uncertainty: President Trump responded within hours by imposing a new 10% global tariff under the Trade Act of 1974, later raising it to 15%. Analysts estimated the ruling could reduce projected 2026 inflation by roughly 0.6 percentage points, but cautioned that continued trade-policy improvisation would sustain uncertainty.

The Fed Pause: The Federal Reserve held its benchmark rate steady in the 3.50–3.75% range at its January meeting, a decision that shaped market expectations throughout February. Minutes released on February 18 revealed a deeply divided committee. Two governors dissented, favoring a quarter point cut. However, the majority opted to hold with inflation running at approximately 2.9%, well above the 2% target.

The producer price index released on February 27 came in hotter than expected, reinforcing concerns about sticky price pressures. Core PCE inflation has hovered near 3%, and the combination of rising oil prices and trade-policy uncertainty clouds the near-term outlook.

The debate was further complicated by the upcoming leadership transition: Chair Powell’s term expires in May. Nominee Kevin Warsh awaits Senate confirmation. Treasury yields declined meaningfully, with the 10-year falling 30 basis points to 3.94%, reflecting growing confidence that inflation was moderating and that rate cuts could resume later in the year.

Iran, oil, and shipping: February ended with a dramatic escalation in geopolitical risk. On February 28, the United States and Israel launched joint military strikes against Iran, targeting leadership and military infrastructure. Oil prices, already climbing on rising tensions, spiked sharply. Brent crude surged roughly to around $80 per barrel; WTI crude had already risen 2.8% during February before the late-month escalation, pushing year-to-date gains above 24%.

Energy stocks benefited directly, and defense names like Lockheed Martin and Northrop Grumman rallied. The broader market sold off, however, as investors weighed the risk of prolonged disruption to the Strait of Hormuz, through which approximately 20% of global oil transits. Gold gained 7.9% in February for its thirteenth monthly advance over the past fourteen months. Thus far, in March, the market has been volatile, partly reflecting geopolitical concerns.

Looking forward

Analysts remain positive on the S&P500, with the 12 month target return being 23.5% above the current index level. Analysts can of course be incorrect. However, analyst predictions are indicative.

We remain constructive on the United States. The geopolitical tensions have created volatility. However, as at the time of writing, the tensions appear contained, at least partly because Iran has alienated itself from most regional players. Disruptions in the Strait of Hormuz could weigh on markets. However, President Trump has signaled moves to support shipping insurance and protect shipments. Historically, geopolitical tensions have generally not resulted in significant adverse market impacts. In March, inflation data will remain important, giving some insight into future fed moves.