Otso Monthly – March 2026

How did we perform?

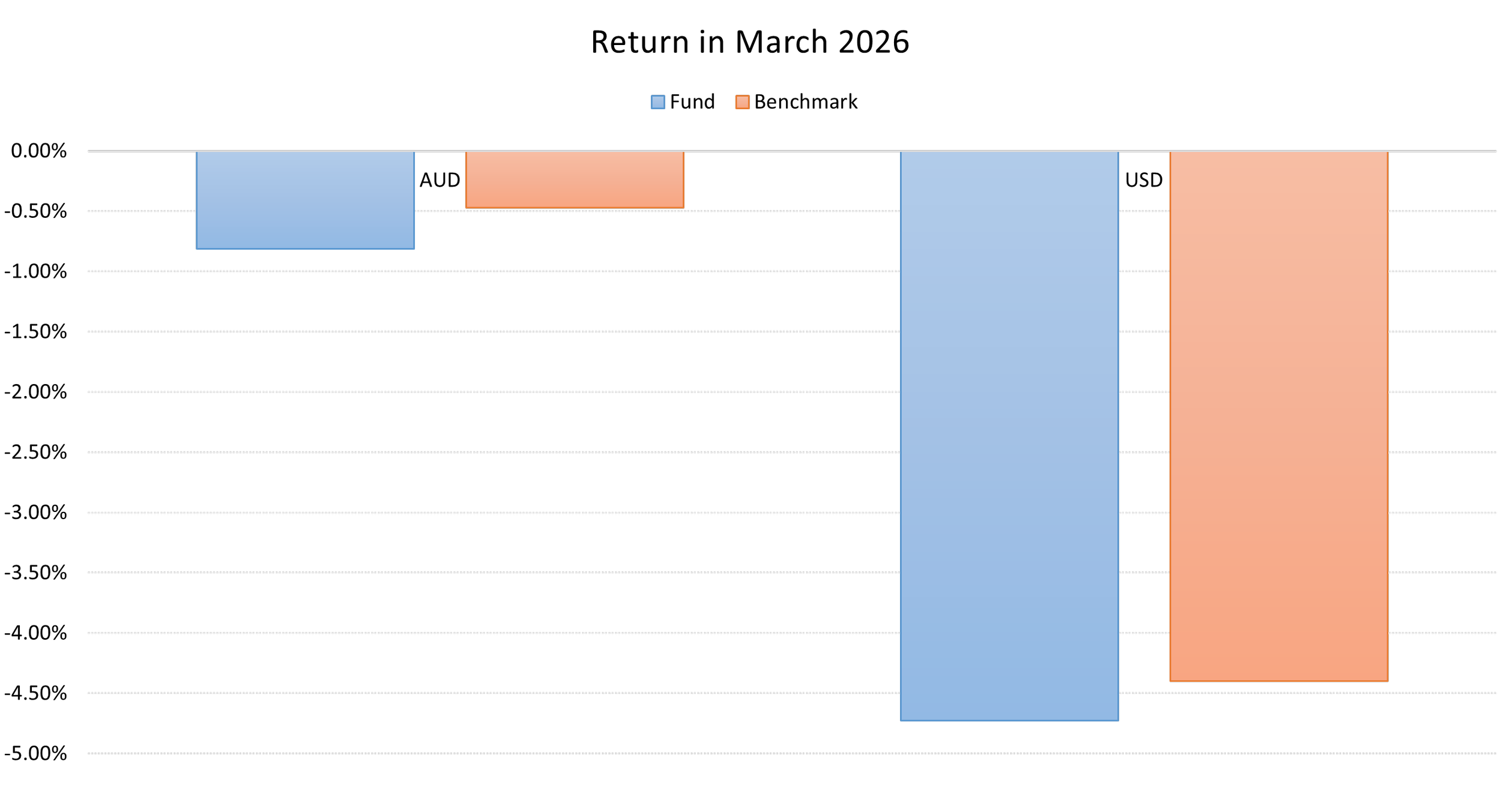

March was a volatile month. The weak US market performance was partly offset by depreciation in the AUD (increasing the value of our US holdings in AUD terms). In USD terms, we fell 4.7% (vs 4.3%, benchmark). However, in AUD terms we declined 0.81% (vs the benchmark falling 0.47%). However, it is important to put this into the context of longer term performance.

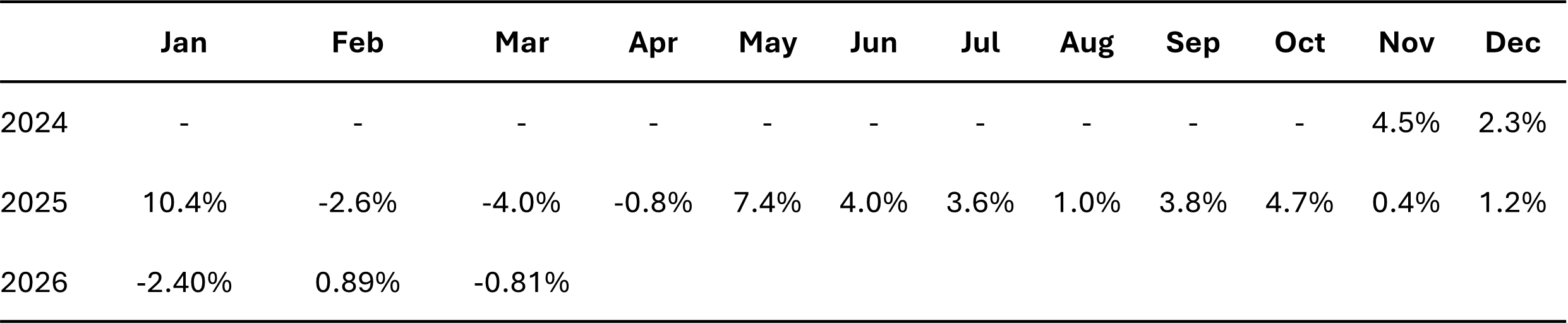

To consider the performance, our long term performance has been solid (see below), with consistently above-benchmark performance.

What happened in March?

March was a stark reminder that markets can be reshaped overnight by events far from any trading floor. After entering 2026 with hopes for cooling inflation and a friendlier Federal Reserve, investors instead spent the month digesting the consequences of the US–Iran war that erupted in late February, and the ripple effects touched nearly every corner of the U.S. equity market.

The Headline Numbers

U.S. stocks closed sharply lower across the board. The S&P 500 fell roughly 5%, the Nasdaq 100 dropped 4.8%, and the Dow Jones Industrial Average declined 5.2%. For the S&P 500, it was the worst month since September 2022, and the index briefly flirted with correction territory before staging a late-month bounce. Volatility, predictably, surged: the VIX peaked at 35.3 in March, its highest reading in many months, though still well below crisis-era extremes.

The Driver: Oil, Hormuz, and Inflation Fears

The dominant story was energy. The Strait of Hormuz (the narrow waterway that handles roughly 20% of the world's oil supply and 20% of its liquefied natural gas) became the focal point of investor anxiety as hostilities disrupted shipping. Brent crude traded above $110–$115 per barrel at various points during the month, while West Texas Intermediate moved well above $100. The energy sector was one of the few bright spots in U.S. equities, while airlines, consumer discretionary names, and other fuel-sensitive industries came under heavy pressure.

The oil shock fed directly into a renewed inflation narrative. With gasoline prices climbing and supply chains under strain, fears of 1970s-style stagflation crept back into the conversation, a toxic mix for both stocks and bonds that hadn't been seriously discussed since 2022.

The Fed Holds, Markets Reprice

The Federal Reserve responded to the new environment with caution. The FOMC voted 11-1 to hold rates steady at its March meeting, with the updated dot plot still pointing to just one rate cut in 2026, and even that has become questionable. The market is now starting to price in no Fed cuts for 2026 at all, a dramatic shift from the optimistic outlook investors carried into the year. Treasury yields reflected the repricing: the 10-year yield jumped from 4% to 4.3% over the course of the month, pressuring long-duration assets and rate-sensitive sectors alike.

An AI Wrinkle

Geopolitics wasn't the only story. Memory chip names like Micron Technology and SK Hynix gave back some of their recent gains as Google's new TurboQuant technology was reported to reduce the memory intensity of AI models, raising questions about whether the AI hardware boom had been over-extrapolated. More broadly, software and SaaS valuations continued to face skepticism as investors wrestled with which business models AI accelerates and which it threatens.

Consumers Wobble, Then Steady

Consumer signals were mixed. The University of Michigan Consumer Sentiment Index dropped sharply to 53.3, its lowest reading since late 2025, weighed down by higher gas prices and market volatility. Yet the Conference Board's measure painted a more resilient picture, edging higher to 91.8 in March, better than the consensus forecast of 87.5. Underlying activity (air travel, restaurant bookings, retail spending) remained surprisingly steady even as headlines worsened.

A Late-Month Rally Offers Hope

The month didn't end on a low note. On March 31, stocks staged their best day since May after reports surfaced that Iranian President Masoud Pezeshkian was open to ending the war with appropriate guarantees. The Dow climbed 2.49%, the S&P 500 gained 2.91%, and the Nasdaq jumped 3.83%. Ten of eleven S&P 500 sectors finished higher, led by consumer discretionary, communication services, and technology, a clear sign that investors were eager to put risk back on at the first credible hint of de-escalation.

Looking forward

The Iran conflict has continued throughout April. There are some signs of progress towards a ceasefire. However, as at the time of writing, talks have faltered. Nevertheless, markets moved positively in early April. Ongoing disruptions in the middle East are negative for markets. And, they do motivate us to carefully manage risk. However, geopolitical concerns tend to have short-lived impacts on markets. We also remain broadly constructive on markets over the long term, meaning that we retain long positions.

Our constructive view is consistent with that of analyst consensus forecasts. Notably, analyst consensus forecasts predict the S&P500 (to which we are benchmarked) will increase slightly more than 20% over the next twelve months. We broadly anticipate further movement towards a resolution in the Middle East and remain long, albeit with risk limits.